True story – Beiler-Campbell Realtors listed a home in the mid $300K’s in the Avon Grove School District for sale. Pictures were taken, rooms were measured, and the listing went on the market on a Friday. After multiple showings and offers, the home was under contract within 24 hours of listing, at above asking price. Weary home buyers see this scenario repeated every week. It’s not your imagination that there are less homes on the market for sale. There are close to 20%* less homes for sale in our region today than 6 years ago. Combine that with an increased number of buyers and it creates a fast-paced market. So, what is bringing so many buyers to the real estate market?

HOME RE-EXAMINED

During the pandemic lock down, “HOME” became more important than ever. Things like security, comfort and living space became priorities. The desire for a place to call your own increased and buyers decided not to wait to buy a home that checks all the boxes.

STILL HISTORICALLY LOW INTEREST RATES

The current low interest rates allow home buyers to buy a larger home and enjoy lower monthly payments. This also encourages renters to become buyers - in southeastern PA, rent prices are comparable to a mortgage payment.

NOTHING NEW

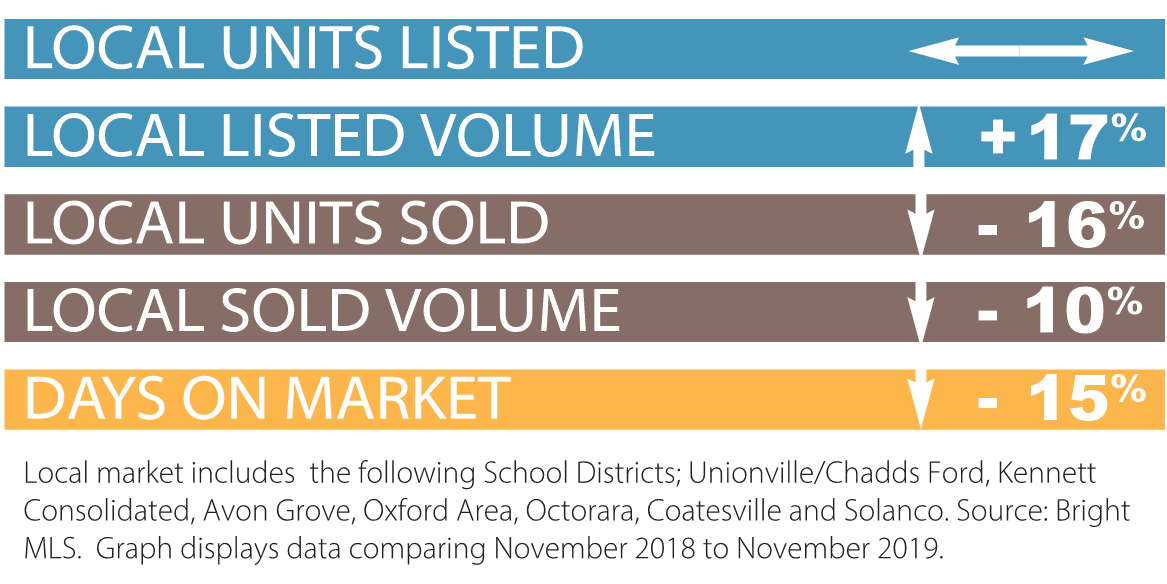

In 2019, southern Chester, Lancaster and Delaware County’s stable job market, thriving economy and low interest rates created a surplus of buyers. Last year’s house hunters that didn’t find their home are still looking this year.

REMOTE WORKING CHANGES PARAMETERS

Telecommuting allows people to live further away from their office. This leads buyers to move to a less populated area and take advantage of purchasing more home for a better price than in urban areas. Realtor.com found that in the second quarter of 2020, 51% of people from urban areas using their site to shop for homes were looking in the suburbs.

MORE PLAYERS IN THE GAME

There's been an influx of millennial home buyers as older millennials have had some time to grow in their careers and pay off student loan debt. If a home is considered in the entry-level or mid-level price range, interested buyers are eager to move quickly.

The moral of our opening story? If you are thinking of moving, now is a great time to sell your home. Listing locally experienced Beiler-Campbell Realtors will ensure your transaction is conducted smoothly and ethically.

MORTGAGE INFORMATION

*Statistics from BRIGHT MLS on 9/8/2020 based on residential homes for sale in Unionville-Chadds Ford, Kennett Consolidated, Avon Grove, Oxford, Coatesville, Octorara and Solanco School Districts.

*Statistics from BRIGHT MLS on 9/8/2020 based on residential homes for sale in Unionville-Chadds Ford, Kennett Consolidated, Avon Grove, Oxford, Coatesville, Octorara and Solanco School Districts.